Water sector moves towards larger and more complex PPPs

Writing exclusively for Energy & Utilities, Dr Corrado Sommariva discusses how public-private partnership (PPP) projects in the region's water sector are becoming increasingly multi-faceted and complex

In the past, public-private partnership projects (PPP) in the GCC were mainly focused on production and treatments in the water industry. For desalination plants, the battery limits were confined to suction or delivery flange of the export pump pipe a few meters downstream of the desalination plants.

Likewise, for sewage treatment plants: raw sewage influent in and treated sewage effluent and sludge out. It was the offtaker’s, rather than the developer’s, concern on how to manage the downstream part of the production or treatment system.

Today, we see long distance pipelines and treated sewage effluent (TSE) storage facilities distributing the TSE effluent of the treatment plant attached to the ISTP in Medina; we see large concession agreements mainly for zero carbon development facilities where the developer is required to provide a technical solution comprehensive of water, power energy storage, district cooling sewage treatment and waste management.

This seems to indicate the prelude of a different way of doing PPPs whereby PPPs are increasingly becoming multi-faceted with limits of responsibility that do not stop at the plant outlet pipe but also include networks, transmission distribution storage and other assets in the value chain.

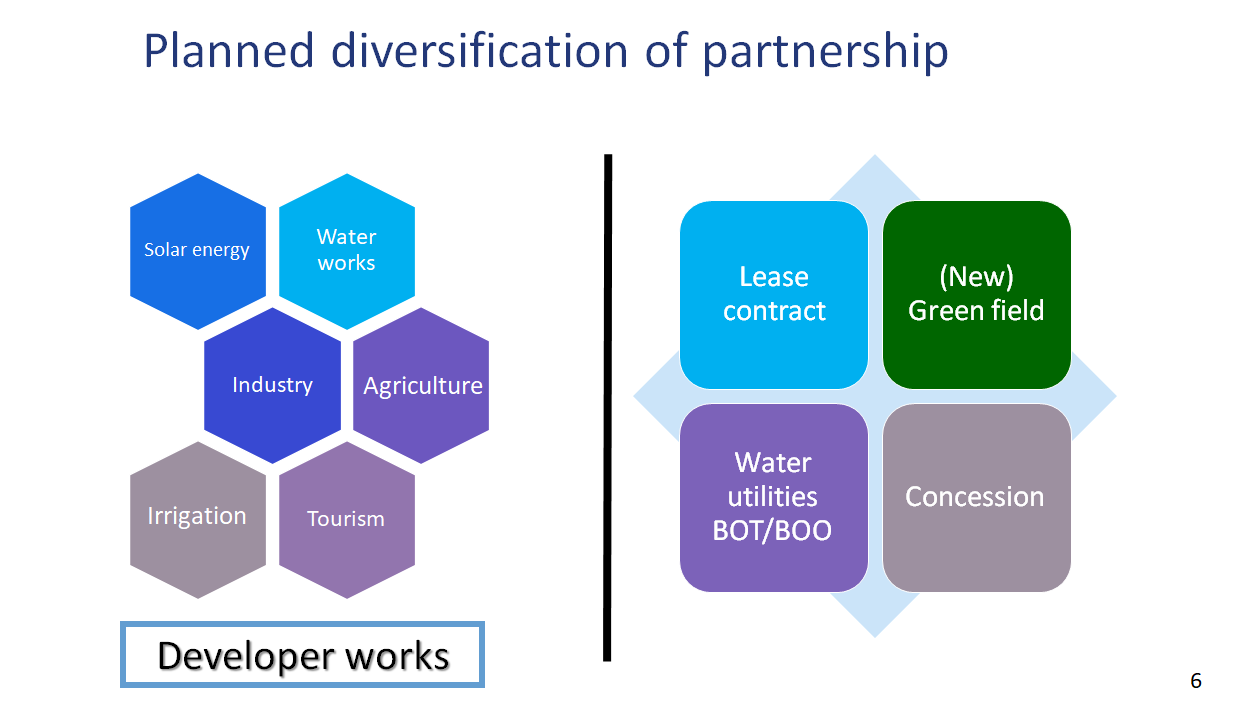

Saudi Water Partnership Company (SWPC) is one of the first companies to announce a planned diversification of partnership, as indicated in Figure 1 below (courtesy of Amer Alrajiba VP Capacity Planning & Analysis PPP Saudi Arabia Diggi conference) where developer works would encompass the all aspects of the sector - including agriculture, irrigation, tourism. This approach is happening now on more and more projects.

Figure 1: planned diversification of partnerships

What happens to the tariff ?

As the range of possibilities for private sector participation is much wider and stem from integrated power (solar PV) and water generation and sales with the possibility of including energy storage for a sustainable water supply, the question arises, what is going to happen to the tariff? Is this going to limit PPP participation only to giants in the industry which have in-house engineering and construction competencies, not only in the water sector but are capable of encompassing diversified disciplines and sectors? Most importantly: will tariffs go higher? Or will they go even lower?

Risks and opportunities for additional revenue streams and call for cooperation

Since the public sector will try to engage the private sector into aspects that are presently handled outside the PPP battery limits, the complexity of the deals most probably will increase. Previous attempts by the concessionaires to involve the private sector into sales to the public have not been successful. The difficulty in fee collection and the risks of non-revenue water in the GCC market poses a risk that currently developers are not prepared to deal with.

On the other hand, as deals become larger, there could be more opportunities for optimisation with secondary and tertiary revenue streams for developers and potential for circular economy via the beneficial use of TSE and sludge for either agriculture or waste to energy or bio methanation purposes.

Since the public sector has been primarily concerned over the last 20 years to ensure comprehensive coverage of the network connection, these two elements - beneficial use of sludge and full TSE reclamation - of the wastewater treatment industry have been somewhat undermined to date.

It is a commercial reality that large flows of TSE are dumped, rather than being further treated and reclaimed for non-domestic applications. This occurs because TSE has no buyers and no commercial value and there are no incentives to use it. The same happens with the sludge which is currently for the majority of the cases dumped to land fill. Along with the decrease of renewable water, we are witnessing a constant increase of wastewater which is now seen as a liability to get rid of at the lowest possible cost. In the same way as waste needs to become the technological and biological nutrient store for future, wastewater also needs to become the new water source for the future. This imposes the need to increase the waste water reuse and reclamation. If the concept of cradle to grave is applied to solid waste, then in the case of water this is an essential requirement for sustainable future.

Along with the inherent energy, nutrients and resources in the wastewater stream can be upcycled, recovering for beneficial use nitrogen, organic carbon, phosphorus and other elements precious to the biosphere.

Gradually in Europe, industry is discovering that the value of struvite as a biological phosphorus-rich fertilizer is gaining commercial momentum versus chemical fertilisers, but the possibilities offered by nutrient recovery are endless and fully in reach of technology today.

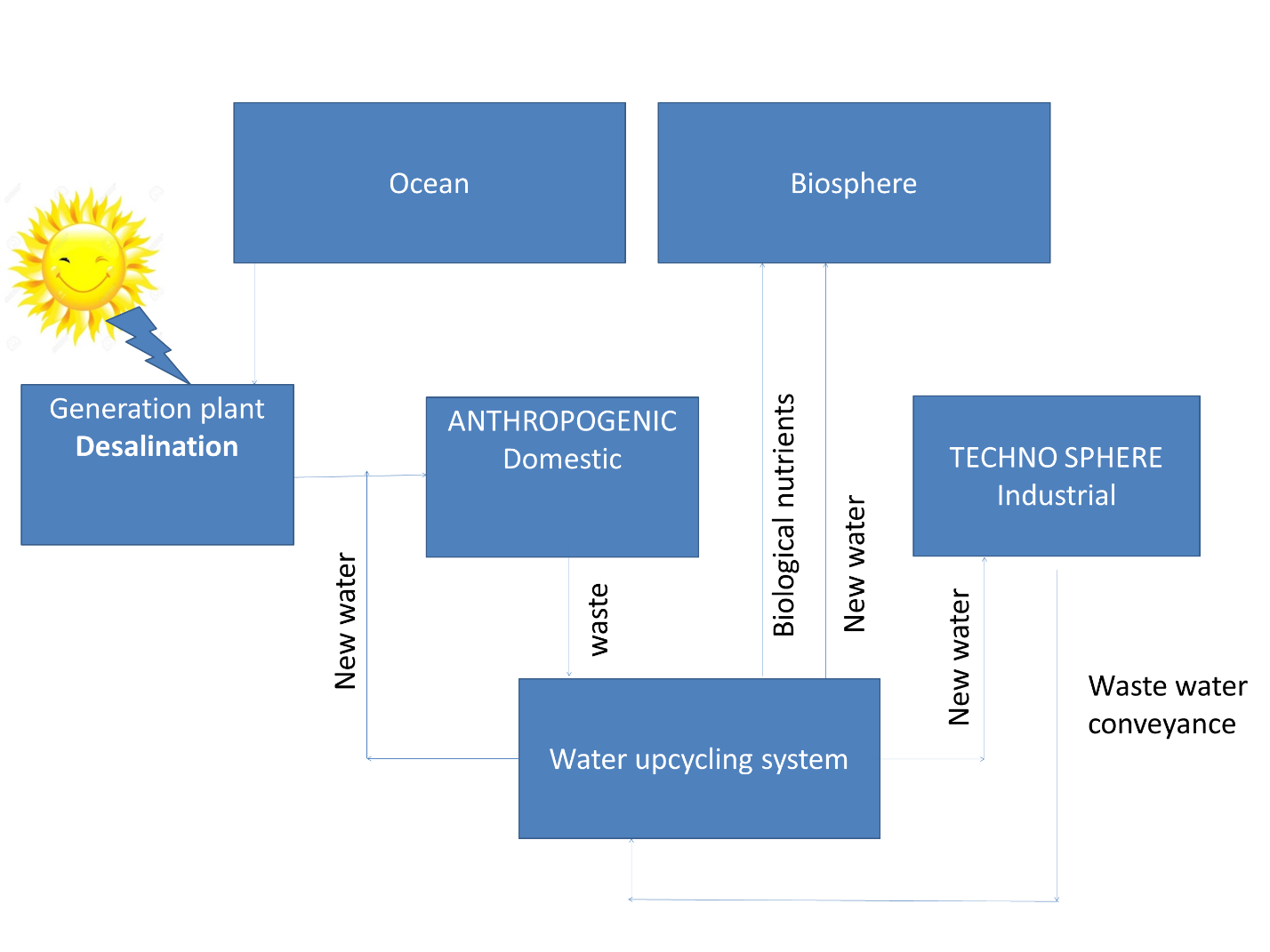

In this perspective a revenue associated to the commercialization and beneficial use of sludge could present an additional revenue stream to the developer and offer several opportunities for optimisation and better use, particularly in the frame of a circular economy pattern as shown in Figure 2 below (Corrado Sommariva : Sustainability a way to abundance).

Figure 2: circular economy pattern

Neither the public nor private sectors can do this alone; the right partnership would ideally see a public sector participation to the risks associated to the development these patterns particularly with regard to the scheme for tariff collection from public users and incentives towards a circular economy. Technology can now offer the possibility to upcycle water through advance water treatment systems. These processes are industrially well proven, can be energy negative (therefore can produce rather than require energy from wastewater) and can further produce energy by enhancing the photosynthetic process.

Written by Dr Corrado Sommariva, CEO of Sustainable Water and Power Consultants (SWPC)

Energy & Utilities - Middle East and Africa Market Outlook Report 2024.

This must-have report for industry players offers a thorough understanding of the latest developments, challenges, and opportunities in the region, supported by data, analysis, and expert insights.

E&U Podcast

Subscribe to our Market Talk podcast for the latest on the key issues and trends in the energy and utilities sector